Buying guide

Mortgage holidays: Can I take one and what will it cost me?

In some cases you may be able to take a break from mortgage repayments. Here’s everything you need to know.

AI summary

A mortgage holiday offers a temporary break from home loan repayments for up to six months if you're facing financial hardship. However, it should be a last resort as it's a repayment deferral, not a free pass.

Interest continues to accrue and is added to your loan balance, increasing the total cost of your mortgage and potentially your future repayments. Consider alternatives first, like interest-only payments or extending your loan term. Contact your lender to apply and seek free advice from Money Talks.

What is a mortgage holiday?

Applying for a mortgage holiday in NZ: Two steps

A mortgage holiday will increase the overall cost of your loan

Everybody needs a break every now and then.

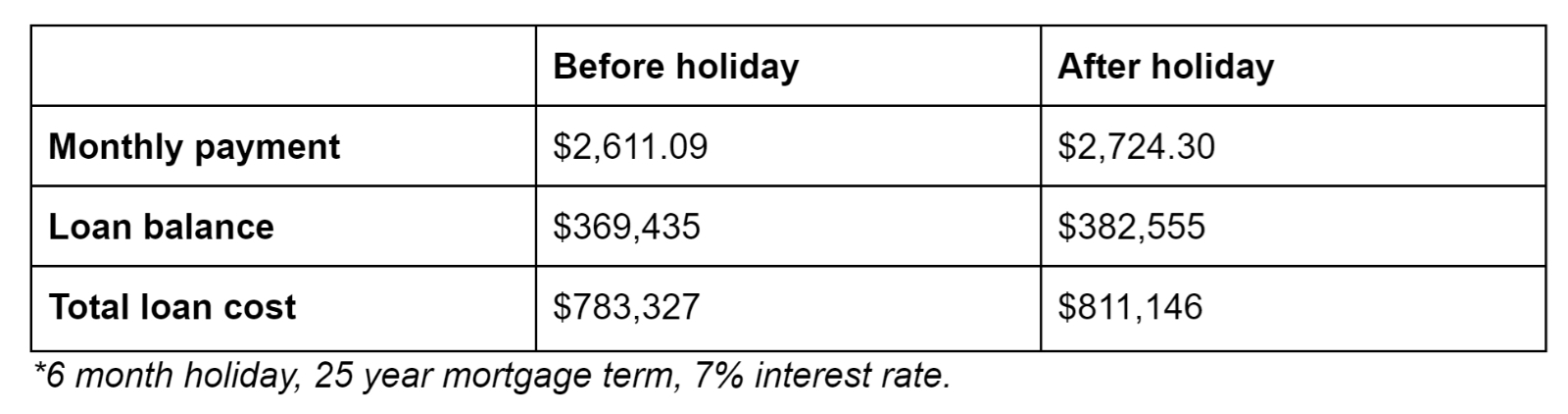

How much more could a mortgage holiday cost me?

Example of mortgage holiday extra costs

Alternatives to a mortgage holiday

Reducing your mortgage repayments to a manageable level

Making interest only payments

Extend your loan term temporarily

Consolidate high interest loans

Refinance and get cash back

When something unexpected happens there is help available to make sure you can keep your home.

Making a plan for when your mortgage holiday ends

Get free financial advice

Author

Discover More

Historic home saved from demolition and turned into $6m waterfront paradise

A rescued Remuera villa is now a $6m-plus Mahurangi Harbour retreat with rich history and waterfront living.

.jpg)

Spotlight on Canterbury, local property market insights

Trade Me data shows Canterbury defying the property cooldown, with high demand for big homes and great townhouse deals.

Search

Other articles you might like