Buying guide

Understanding leverage: a beginner’s guide

Don’t let jargon get in the way.

AI summary

This guide explains leverage in property investing—borrowing money, like a mortgage, to purchase an asset.

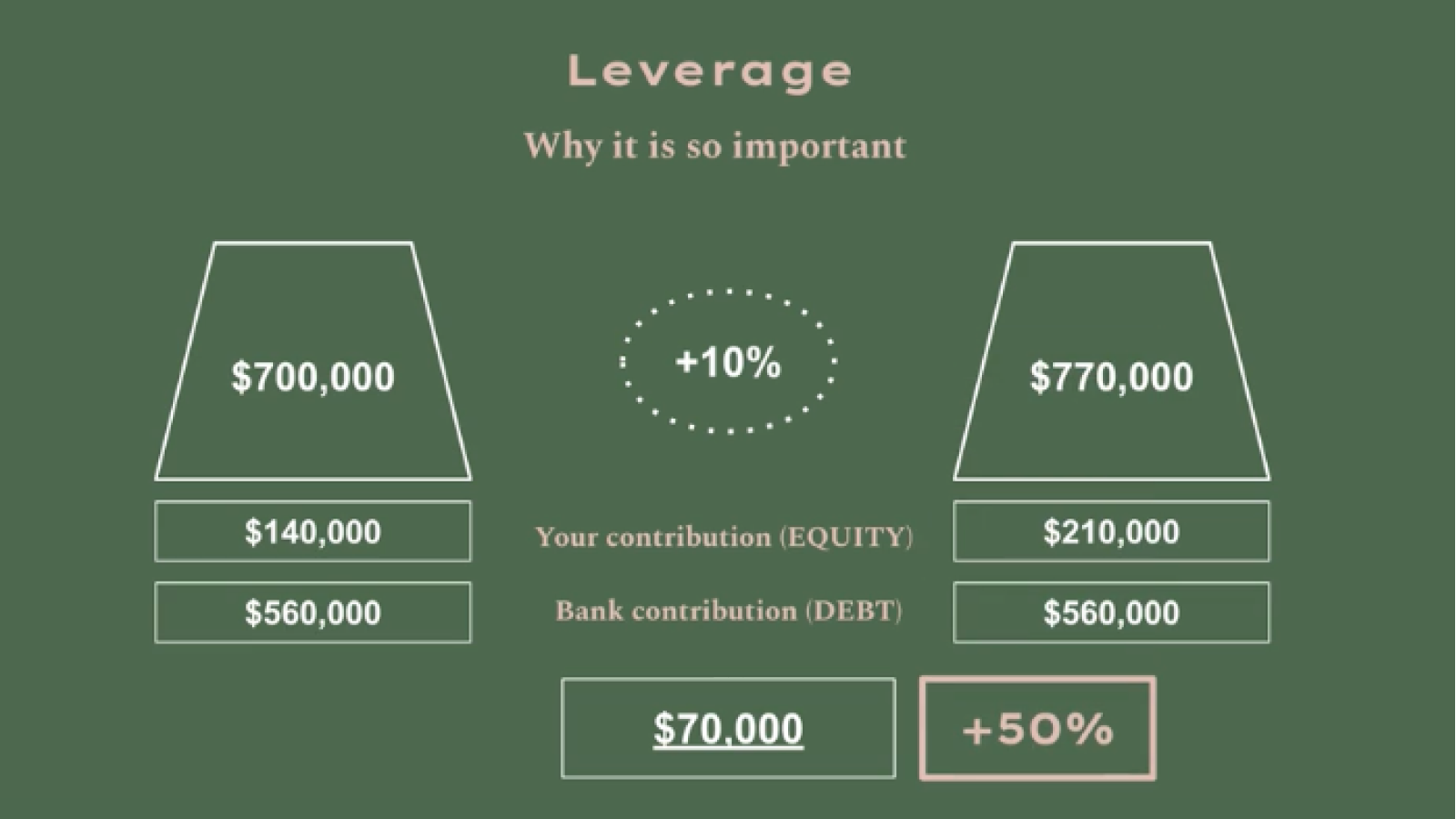

Leverage magnifies returns, meaning a small rise in property value can create a large percentage gain on your deposit. Conversely, it also magnifies losses if prices fall. These are 'unrealised' until you sell.

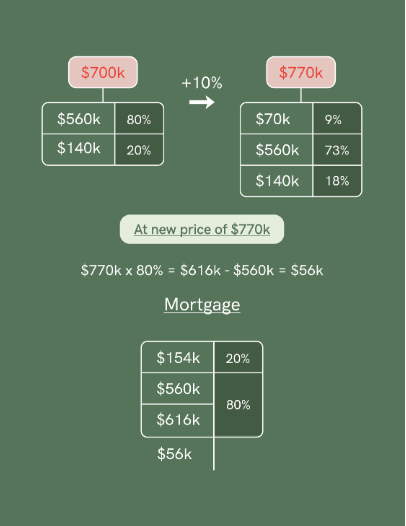

Increased equity from rising values can also be borrowed against for renovations or a deposit on another property, subject to bank lending rules like LVR restrictions.

Image source: www.reinz.co.nz New Zealand House Price Index - June 2024

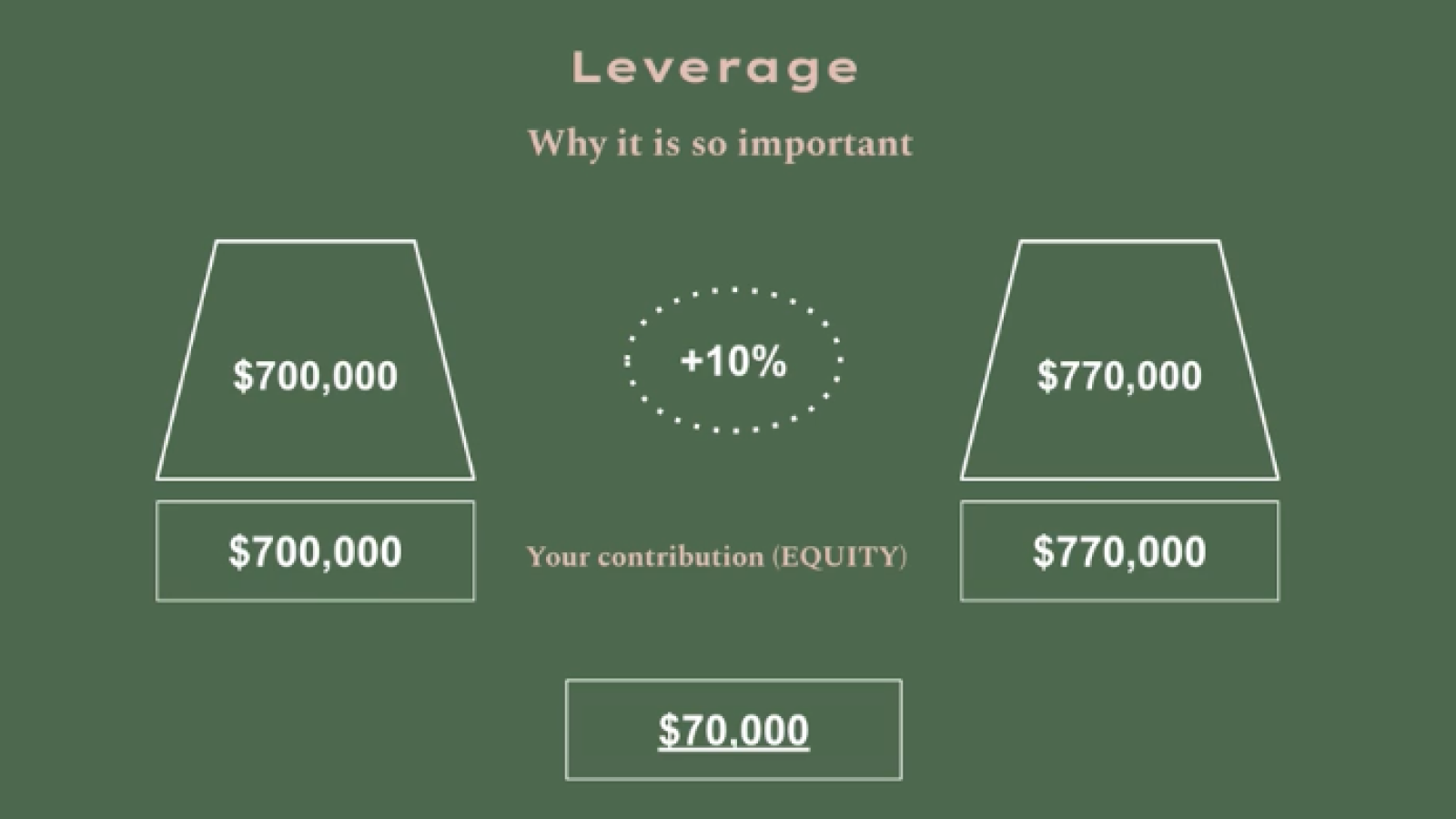

Example #1: No leverage

Example #2: With leverage + property prices RISE

Example #3: With leverage + property prices FALL

Realised vs. unrealised leverage

The attractiveness of leverage

Financial Disclaimer

Author

Search

Other articles you might like