Feature article

Where will your deposit come from?

Your deposit does NOT have to all come from one place.

AI summary

Building a house deposit in New Zealand is achievable by combining funds from various sources. Don't be discouraged by high prices, as 5-10% deposit options and government schemes are often available.

Primary sources for your deposit include:

- KiwiSaver: A popular choice, accessible after three years of contributions.

- Personal savings: Grown through term deposits, cash funds, or investments.

- Parental help: Often provided as a gift or a formal loan (DOAD).

Creative methods like selling items or negotiating a pay rise can also boost your funds.

“Comparison is the thief of all joy”

Where will your deposit come from?

1. KiwiSaver

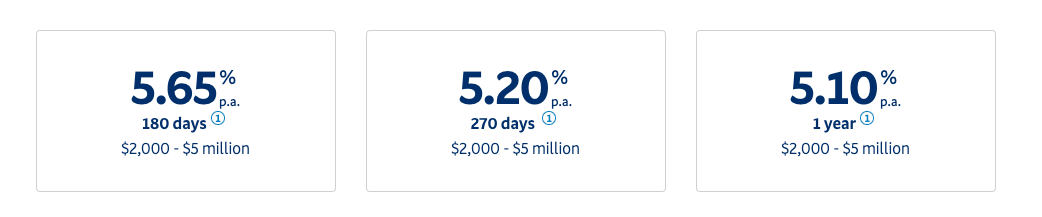

2. Savings

BNZ featured term deposit rates 2024

Kernel Fund Performance as of August 2024

3. Bank of mum and dad

4. Other things

Financial Disclaimer

Author

Discover More

A whole Lot-to love: what a $35m Powerball win buys in luxury property

How to spend $35 million: The ultimate New Zealand luxury property shopping list

'There's something old school romantic about it': The $299k crib that stole their hearts

A charming 1960s seaside crib with harbour views and vintage character is on the market for $299,000.

Search

Other articles you might like